How to write a declaration yourself. Tax return information

This article will be useful to those individuals who do not know how to correctly compile for 2019.

Download declaration form 3-NDFL for 2019We will talk about the form, design methods and rules in accordance with which a document of this kind should be filled out. Also below are links to free downloads of different tax return options.

- A sample form 3-NDFL for 2017 is available here.

- You can download a blank tax return form

- The program for filling out the declaration form is located.

In 2019, taxpayers fill out a declaration either if they want to reimburse overpaid taxes from the state budget (receive a tax deduction) or if they have debts to the tax office.

And sometimes a document is drawn up and submitted for verification so that an individual can report unexpected profits (for example, when selling real estate or receiving income through an investment account).

It should be noted that the Federal Tax Service approved a special declaration for the declaration, the last amendments to which were made on October 25, 2017. The document confirming the validity of this form is order MMV-7-11/522.

How to compose

The process of filling out a tax return can occur in different ways, and each taxpayer has the right to independently choose which of the following options to use:

- Submit on paper. The first method is to enter data by hand into form 3-NDFL, which can be downloaded from the link above. In this case, the taxpayer needs to decide which pages of the form he must fill out and enter reliable information into them without errors.

Complete on the computer.Tax legislation has approved specially developed software for filling out the 3-NDFL declaration, which you can either download or enter information into online. After the programs will have all required information has been completely entered,it must be sent to the tax service for verification.

If an individual who needs to fill out form 3-NDFL, if there are any difficulties regarding this issue, we recommend asking them to the tax inspector working in the inspectorate at the place of its registration.

Page classification

The tax return form begins with a title page, in which basic information about the applicant for the deduction must be entered, then there are sections one and two, intended for entering all kinds of calculated values related to the taxable base, andThese pages are already followed by Sheet A, which is dedicated to income information.

All these sheets must be filled out by an individual in any case, regardless of the purpose for which he submits a declaration (if the taxpayer’s profit comes from foreign countries, then sheet B must be completed).

"IN " -sheet required for written reporting on the profits of individuals engaged in a special type of activity,which includes such professions asentrepreneurs, farm managers, private lawyers and notaries, as well as some others.

"G" - on On this page, in the corresponding paragraphs, income is displayed from which personal income tax is not deducted by law. For example, this is a one-time financial assistance given to a taxpayer for the birth of a son or daughter, compensation provided by managers to former employees who are disabled, gifts received from entrepreneurs or enterprises, and some other types of profit.

"D1" and "D2" -both sheets are intended to indicate information relating to financial transactions with property.Only sheet D1 is filled out if the taxpayer is purchasing a plot of land, a house, apartment or room (or investing money in the construction of listed real estate), and sheet D2 is completed if he has completed a transaction to sell the property.

"E1" -this page is included in form 3-NDFL so that individuals can qualify for standard tax discounts (these are monetary compensations that are provided to preferential categories of citizens orparents as assistance in providing for their children) or social deductions (tax reimbursement for expenses associated with paying for medical procedures and purchasing medicines, with payments for training , as well as with charitable, pension and insurance contributions).

"E2" - sheet with a similar designation is needed for individuals applying for a reduction in the tax base in accordance with subparagraphs 1.4 and 1.5, which are part of Article 219 of the Tax Code. That is, these are all kinds of tax discounts that are given to investors who have overpaid personal income tax.

"AND" -This page is required to be completed by those taxpayers who are legally entitled to receive professional tax compensation. This category of individuals includes not only individual entrepreneurs and personsthose who receive profit as a result of performing civil law tasks fixed in special agreements, but also taxpayers whose income is related to copyright objects, as well as private lawyers.

"Z" -this sheet takes up several pages of the 3-NDFL form and is dedicated to income related to m with the implementation of various property transactions using securities, as well as the profit that comes to taxpayers from transactions with derivative financial instruments (an agreement fixing the rights relating to the underlying asset).

"AND " -This page is necessary for conducting taxable settlement operations on profits received by individuals who participate in investment partnerships.

How to draw up a declaration correctly

If the declaration is filled out on paper, be sure to staple sheets , thereby eliminating the loss of one orseveral of them. Stapling should be done in areas of the pages where there is no information or images. In addition, the format and color of the print are important. Use only black or blue and never printseveral pages on one sheet at the same time.

Also, in the process of filling out a tax return, it is worth considering that all specified information must have documentary evidence. That is, the passport information written on the title page must fully correspond to the data displayed in the copy of the passport attached to form 3-NDFL, the amount of expenses must correspond to the amount indicated in the payment documentation, and so on.

In addition, if the applicant for a deduction doubts his rights to reduce the tax base, we recommend that you read Articles 218-221 of the Tax Code to clarify the situation. It is also very important to comply with the deadline for submitting the 3-NDFL form for consideration and not to forget about such a concept as the statute of limitations for deductions.

How to fill out deductions in the 3-NDFL declaration? This article, as well as a selection of materials from our website, will help answer this question. Filling out tax deductions in 3-NDFL occurs according to special algorithms, taking into account the conditions established by the Tax Code of the Russian Federation for their application. Let's consider the algorithm for filling out the 3-NDFL declaration for deductions.

What are tax deductions in the 3-NDFL declaration, why are they needed and who can claim them

For the purposes of filling out 3-NDFL, a tax deduction is usually understood as a decrease in the income received by an individual or individual entrepreneur, on which income tax is paid. The same term denotes the return of previously paid personal income tax in situations provided for by the Tax Code of the Russian Federation (in connection with the purchase of property, expenses for training, treatment, etc.).

A person who:

- is a citizen of the Russian Federation;

- has income subject to personal income tax (13%).

Deductions allow you to reduce the tax burden on an individual (reduce income tax payable or return part of previously paid personal income tax).

The Tax Code provides for 5 types of deductions:

- standard (Article 218 of the Tax Code of the Russian Federation);

- property (Article 220 of the Tax Code of the Russian Federation);

- social (Article 219 of the Tax Code of the Russian Federation);

- professional (Article 221 of the Tax Code of the Russian Federation);

- associated with the transfer of losses from transactions of individuals with securities (Article 220.1 of the Tax Code of the Russian Federation).

For current changes in the legislation on tax deductions for personal income tax, see the heading of the same name "Tax deductions for personal income tax in 2018-2019"

Each deduction has its own characteristics and can only be applied taking into account the conditions specified in the Tax Code of the Russian Federation. Next, we will tell you how to fill out certain types of deductions in the 3-NDFL declaration.

NOTE! The declaration for 2018 must be submitted using the new form from the Federal Tax Service order dated October 3, 2018 No. ММВ-7-11/569@. You can download the form.

How to fill out standard deductions in 3-NDFL

Standard tax deductions are provided to certain categories of individuals (“Chernobyl survivors”, disabled people since childhood, parents and guardians depending on the number of children, etc.).

Find out more about standard deductions.

In 3-NDFL, information about standard deductions is provided from the data in the 2-NDFL certificate and is necessary for the correct calculation of the amount of personal income tax (its refundable part or paid to the budget).

Let's look at filling out information in 3-NDFL about standard tax deductions using an example.

Example 1

Stepanov Ivan Andreevich bought an apartment in 2018 and decided to return part of the personal income tax. To do this, he filled out 3-NDFL using the “Declaration 2018” program posted on the Federal Tax Service website.

To enter information into 3-NDFL after filling out the initial data (about the type of declaration, the Federal Tax Service code, personal data and other mandatory information), in the “Deductions” section, I. A. Stepanov ticked the following boxes:

- “provide standard deductions”;

- “there is neither 104 nor 105 deduction” (which means that Stepanov I.A. has no right to a deduction of 500 or 3,000 rubles per month provided to the categories of persons specified in paragraph 1 of Article 218 of the Tax Code of the Russian Federation);

- “the number of children per year did not change and amounted to” - from the list Stepanov I.A. chose the number “1”, which means that he has an only child.

For the Ministry of Finance’s opinion on “children’s” deductions, see the message “Child from a first marriage + child of a spouse + common: how many deductions is an employee entitled to?” .

What the “Deductions” section looks like after filling out, see the figure:

In order for the program to calculate the amount of standard deductions and generate the necessary sheets in 3-NDFL, Stepanov filled out another section - “Income received in the Russian Federation” - as follows:

As a result of filling out these sections in the declaration by the program, Appendix 5 was formedwith information on the total amount of standard tax deductions provided to Stepanov I.A. at his place of work. The program calculated the total amount of deductions taking into account the limit established by the Tax Code of the Russian Federation on the amount of income within which standard “children’s” deductions are provided.

Fragment of completed application 5For information on the total amount of standard deductions and the number of months of their provision, see below:

Explanation of information in Appendix 5:

- deductions for 1 child in the amount of 7,000 rubles. (RUB 1,400/month × 5 months);

- deductions are provided for 5 months. — the period from January to May 2018 (until the cumulative income from the beginning of the year did not exceed 350,000 rubles).

The article will tell you about the nuances of registering 3-NDFL “Sample of filling out tax return 3-NDFL” .

Reflection of social deductions in 3-NDFL (together with standard deductions)

The Tax Code of the Russian Federation provides for 5 types of social tax deductions (see diagram):

Let's change the conditions of the example (while maintaining the data on income and standard deductions entered into the program) described in the previous section to clarify the rules for filling out social deductions in 3-NDFL.

Example 2

Stepanov I.A. paid for his advanced training courses in 2018 in the amount of 45,000 rubles. In the 3-NDFL declaration, he declared his right to a personal income tax refund in the amount of 5,850 rubles. (RUB 45,000 × 13%).

To reflect the social deduction in 3-NDFL, Stepanov I.A. filled out the “Deductions” section in the following order:

- checked the box “Provide social tax deductions”;

- in the subsection “Amounts spent on your training” indicated the amount of 45,000 rubles;

- I left the remaining fields blank.

After entering the data, the completed “Deductions” section in the program began to look like this:

Dedicated to social and standard deductions, Appendix 5 of the 3-NDFL declaration began to look like this (reflecting the amount of standard and tax deductions):

For new tax deduction codes, see the article “Tax deduction codes for personal income tax - table for 2018 - 2019” .

Nuances of using the right to deduction (year of start of use, deductions for previous years, where 3-NDFL with deductions is submitted)

An individual wishing to use his right to deduction must take into account that:

1. For 2018, 3-NDFL is submitted in the form approved by Order of the Federal Tax Service dated October 3, 2018 No. ММВ-7-11/569@. You can download the form.

2. The year in which the deduction began to be used is the year for which the personal income tax was first returned.

3. The need for deductions for previous years may arise if an individual returns personal income tax for several years (for example, when buying a home in installments) or the individual learned about his right to a deduction later than the period of obtaining the right to it.

Cm. “Tax deduction when buying an apartment with a mortgage (nuances)” .

4. Separate tax deductions can be obtained both from the tax office and from your employer. In the first case, 3-NDFL must be submitted to the inspectorate at the place of residence.

Results

A tax deduction in the 3-NDFL declaration is reflected if the taxpayer has income taxed at a rate of 13% and he belongs to the categories of persons specified in the Tax Code of the Russian Federation who are entitled to receive a deduction.

Deductions in 3-NDFL are reflected on special sheets depending on the type (standard, social, property, etc.). A program posted on the Federal Tax Service website will help you fill out the declaration without errors, identifying errors and calculating the tax to be refunded or paid.

Citizens of the Russian Federation: business entities, civil servants, employees, persons who have received additional income - must submit tax returns in accordance with the law and established standards of the Tax Code of the Russian Federation.

Tax return for tax paid

Taxpayers declare in the prescribed form the income received, taking into account benefits and discounts, during a certain reporting period. Taxes, according to the established rate, are paid by citizens of the Russian Federation - private entrepreneurs (IP); organizations (budgetary, commercial and charitable); entities operating on the territory of the Russian Federation, including religious, educational, etc. Enterprises with zero income are not exempt from reporting.

Types of declarations:

- VAT return;

- tax return: income tax;

- personal income tax;

- transport tax;

- tax return: property tax;

- land tax;

- water tax;

- excise tax;

- mineral extraction tax (MET);

- tax return under the Unified Agricultural Tax (unified agricultural tax);

- imputed income (UTII).

Declarations are submitted for tax and reporting periods within the time limits established by the Tax Code.

Tax return according to the simplified tax system (KND-1151085)

Individual entrepreneurs are required to submit a tax return to the State Tax Inspectorate for the past calendar year with a deadline of April 30. For a certain period (for example, a quarter, half a year), reports are submitted by the 20th of the next month.

A tax return under the simplified system contains information: full name (including tax identification number) of the entrepreneur or name of the organization; taxable period; tax rate; OKVED code; OKATO; budget classification code (KBK); amount of insurance premiums. Provided by the State Tax Inspectorate in a single copy.

A simplified zero tax return, if there was no cash flow in the reporting period, is filled out as follows: title page; lines 001, 010, 020, 201; the rest is dashes. Rented quarterly.

Tax return for the sale of a car

The amount that the owner receives from the sale of a car is one of the components of income for individuals. Provided that documents on the initial acquisition of property are preserved, this amount can be deducted from the income received. You must pay tax on the balance according to the rate. Documents confirming the purchase may be: receipts; cash receipt orders; receipts for depositing cash into the bank into the seller’s account; a receipt confirming receipt of funds by the seller. A purchase and sale agreement, if it does not indicate the purchase amount, is not such a document.

It is important to know and comply with the laws and rules of civilized business: “Deadline for filing the 3rd personal income tax return”?:

Calculation of the tax amount in the personal income tax return

1. Tax is not paid in the following cases:

- the owner has used the car for more than three years;

- the initial purchase amount of the car is greater than the sale amount;

- if the sale amount is less than 125 thousand Russian rubles.

2. In other cases, the tax is calculated using the formula: amount of car sales – 125,000 x 13%. The resulting number is rounded according to generally accepted rules to whole numbers.

Tax return when purchasing an apartment

Housing can be purchased either at once or through lending from financial institutions. In such cases, a loan and mortgage agreement is concluded.

The mortgage tax return contains the following information:

- passport and TIN of the owner,

- certificate 2-NDFL about income, including wages,

- contract of sale of an apartment,

- certificate for real estate on the secondary market,

- share participation agreement,

- acceptance certificate from the developer for real estate in a new building,

- seller's receipt or document confirming payment.

The tax office issues tax deductions in accordance with the following documents: payment slips confirming payment of expenses, including receipts for receipt orders; seller's receipt; bank statements on mortgage repayments; acts of purchase of materials and sales receipts; loan agreement.

Tax return when selling an apartment

The declaration is submitted before the first of May following the year in which the income from the sale of real estate was received.

Filling out a tax return for an individual takes into account the following points:

- if the sold apartment belonged to the owner for three or more years, the income is not taxed and the declaration is not submitted to the State Tax Inspectorate;

- if the apartment is sold for no more than one million Russian rubles, income tax is paid minus this amount;

- if income exceeds one million Russian rubles, the tax rate is 13%;

- if a share is sold, each of the co-owners fills out a declaration indicating the amount of income; It is necessary to distinguish between a share in property rights and a share allocated in kind.

In order to protect yourself and your business from unnecessary consequences and problems, it is important for every entrepreneur to know what is: “Personal Income Tax Calculation”?:

In order to protect yourself and your business from unnecessary consequences and problems, it is important for every entrepreneur to know what is: “Personal Income Tax Calculation”?:

Tax return for individuals

Served in the following cases:

- filling out a tax return for an individual is provided in case of receiving income from the sale of property;

- tax residents of the Russian Federation who have not resided in the country for the last twelve months or 183 days; exception - military personnel serving and receiving income outside of Russia;

- individuals who received any income during the year but did not pay taxes for various reasons;

- individuals who received winnings from a lottery, sweepstakes, casino or slot machines;

- heirs or legal successors of scientific works, literary works, etc.;

- individuals who received the fee;

- a gift tax return is filled out by persons who received income from other individuals in cash or in kind;

however, if the gift is received from close relatives, no return is filed.

Tax return for single tax

According to Art. 346.19 of the Tax Code of the Russian Federation, a distinction should be made between the tax and reporting periods. In the first case, the period is the calendar year. In the second case: quarter (3 months), six months (6 months), nine months.

“Simplers” transfer advance payments with a deadline of the 25th day of the month following the reporting period, in accordance with clause 7 of Article 346.19 of the Tax Code of the Russian Federation. There is no need to submit tax returns for reporting periods. The procedure for calculating tax depends on the object of taxation chosen by the organization or individual entrepreneur.

Based on the results of the past calendar year, the single tax is transferred to the budget with a deadline of March 31. Individual entrepreneurs are required to make payments with a deadline of April 30. The declaration is drawn up according to the standards approved by Order No. 58 of the Ministry of Finance of the Russian Federation dated June 22, 2009.

Tax return for UTII

UTII is a single tax on imputed income, a tax that is introduced at the municipal level and applies to certain areas of activity.

List of objects subject to UTII:

- domestic services;

- veterinary;

- maintenance; transport services, storage and washing;

- retail;

- public catering;

- outdoor advertising, including in vehicles;

- provision of housing for rent, hotel services;

- provision of land plots and places for trade for rent

The tax rate is about 15%.

Tax return for transport tax

Transport tax is a payment to the regional budget. It is carried out by owners at the place of registration of vehicles in accordance with the standards established by the Tax Code of the Russian Federation.

In accordance with paragraph 1 of Art. 363.1 of the Code, taxpayers who are enterprises and organizations submit a declaration to the INFS after a certain tax period. Section 2 is completed in accordance with each vehicle unit.

Tax return for land tax

In accordance with the order of the Federal Tax Service of the Russian Federation dated October 28, 2011, the declaration is filled out by both organizations and individuals (IP) regarding land plots intended for business activities (for example, farming) and owned by the owners on the right of ownership, as well as on the right of permanent use. They are provided to the NI at the location of the given land plot.

Sections of the declaration:

- title page;

- Section 1: “The amount of land tax payable to the budget”; advance payments in line: 023, 025, 027;

- Section 2: “Calculation of the tax base and the amount of land tax.”

Tax return for civil servants

Based on clause 179.11 of Art. 179 of the Tax Code of the Russian Federation, civil servants are required to submit a tax return indicating their property status, income, expenses, and financial obligations. It is also necessary to provide complete information required by law about the income of family members.

Based on clause 179.11 of Art. 179 of the Tax Code of the Russian Federation, civil servants are required to submit a tax return indicating their property status, income, expenses, and financial obligations. It is also necessary to provide complete information required by law about the income of family members.

The declaration is submitted to the State Tax Service at the tax address of the taxpayer - place of residence. It should be taken into account that a taxpayer can have only one tax address at a time, in accordance with clause 45.1 of Art. 45 of the Tax Code of the Russian Federation.

A tax return can be submitted:

- personally;

- authorized person;

- sent by mail with a mandatory description of the attachment and subsequent notification;

- by email.

Tax return of an individual entrepreneur

Types of individual entrepreneur declarations

- the UTII declaration is submitted quarterly;

- tax return of individual entrepreneur USN;

- excise tax declaration;

- zero declaration is a common form of reporting when doing business;

- land tax declaration;

- transport tax declaration.

The legislation of the Russian Federation provides for the possibility of providing updated declarations with corrected information. Typically, the entrepreneur submits corrections on his own initiative. If the tax authorities determine that there are inaccuracies, an updated form will be provided upon request.

Declaration for obtaining a tax deduction

According to the legislation of the Russian Federation, taxpayers who have purchased real estate or are involved in construction are entitled to a tax deduction. Amounts intended to repay loans received from financial institutions of the Russian Federation are also taken into account,

The procedure for obtaining a tax deduction

STEP #1. You must obtain the appropriate forms from the tax office.

STEP #2. All documents for the relevant property are prepared:

- certificate of ownership;

- contract of sale;

- Act of Handover;

- payment documents;

- documents confirming expenses;

- income certificate 2-NDFL;

- a pre-issued savings book on which deductions will be made.

STEP #3. Filling out the declaration (KND 115020):

- title page;

- Section 6: “The amount of tax that is subject to payment to the budget or refund”;

- Section 5: “Calculation of the total amount”;

- Section 1: “Calculation of the tax base at a rate of 13%”;

- Appendix A: “Income in the Russian Federation taxed at a rate of 13%”;

- Appendix K: “Calculation of standard and social deductions”;

- Appendix L: “Calculation of property deduction.”

If necessary, appendices “G” and “G” are additionally filled out: income from the sale of property, financial assistance from employers, gifts, prizes.

4. The next step is an application addressed to the management of MIFINS of the Russian Federation in your region, which sets out a request for a tax deduction.

5. Tax administration specialists carry out appropriate examination and verification. If the decision is positive, the taxpayer is notified in accordance with the established procedure. The funds are credited to the savings book provided in advance.

It is necessary to take into account that in order to extend the deduction procedure, a tax return is submitted annually to the State Tax Inspectorate: income tax refund.

Tax return for education

If during the period of study the taxpayer worked, which can be confirmed by a 2-NDFL certificate, he has the right to a refund of tax for training (a period of three years, since in earlier periods the tax history is considered outdated). In this case, a declaration is provided: tax deduction for education.

If during the period of study the taxpayer worked, which can be confirmed by a 2-NDFL certificate, he has the right to a refund of tax for training (a period of three years, since in earlier periods the tax history is considered outdated). In this case, a declaration is provided: tax deduction for education.

To calculate the refund, the amount that was paid during the training period should be added and multiplied by 0.13. According to the taxpayer’s application and data from the 3-NDFL tax return, part of the tax paid to the budget is returned.

What does a tax deduction even mean? The taxpayer, according to the legislation of the Russian Federation, has the right to reduce taxable income (wages accrued during the calendar year) by the amount that was paid for his own training. However, it is worth considering that the size should not exceed 120,000.00 Russian rubles. If you paid for the education of several children, then the amount should not exceed 50,000.00 Russian rubles for each child. An educational institution must have the required accreditation and appropriate license. Otherwise, payments will not be made.

Updated tax return

What is this type of reporting? All goods that were imported during the reporting period. Unlike the general VAT return, the taxpayer fills out the form without a cumulative total. That is, only monthly data is taken into account.

In this regard, it is not always possible to correct inaccuracies in the tax return for the reporting periods following the current one. In order to correct incorrect information provided by the taxpayer, an amended tax return must be submitted within the time limits specified by the regulations of the Tax Code of the Russian Federation. For these purposes, there are special lines “Change in the tax base for previously imported goods.”

In what cases is an updated tax return provided?:

- If an error (error) is detected in the application of the VAT rate.

- If an error (error) is detected in determining the tax base, provided that the data for calculating VAT were known on the date of submission of the declaration.

- When exporting goods intended for sale from the territory of the Russian Federation within one month, with subsequent return.

If you provide an updated tax return, you must write a statement about the import/export of goods in which indirect taxes were paid.

It should be taken into account that when returning goods to the Russian Federation, the payer has every right not to provide an updated declaration, accepting the entire amount of tax paid as a deduction. However, an updated declaration must be provided in the event of returning goods, if the initial declaration has not yet been submitted to the Tax Inspectorate.

An updated tax return is not provided:

- If, after calculating VAT for a certain period of time on goods exported from the territory of the Russian Federation, expenses are known that increase the tax base for these items.

- In case imported goods from Russia are returned to the seller within the same month.

- In case of a change in the tax base due to fluctuations in exchange rates at the time of receipt of the goods before the payment deadline.

Tax return for property deduction

This type of deduction includes three components:

- In relation to the costs of building a new house or purchasing real estate on the territory of the Russian Federation (in any region), including land plots for development.

- In relation to the costs of repaying existing interest on targeted loans. It is worth considering that loans can be issued exclusively by Russian financial institutions, as well as individual entrepreneurs. These funds must be spent for their intended purpose - construction or purchase of housing.

- Expenses to repay existing interest on loans (loans) received for the purpose of refinancing for the purchase of housing (apartment, house) or land for development. Including the construction of a residential building. On-lending can be carried out exclusively by Russian financial institutions.

How can I get a property deduction? In case of acquisition or construction of a residential house (cottage), apartment or room, share, land plot for construction. The deduction is made solely in the amount of expenses that were incurred. However, it is worth considering that the amount should not exceed two million Russian rubles, not taking into account previously paid interest on current loans.

VIDEO: Taxes in Russia: how to avoid irreparable mistakes

1.1. Fill out the section “Setting conditions”:

1.2. In this section you must fill in the “Inspection Number” - selected from the attached directory:

If you do not know your inspection number, you can find it out by using the on-line service “Address and payment details of your inspection” on the Federal Tax Service website: https://service.nalog.ru/addrno.do

All other parameters specified in this sectionare defined for an individual by default. If You are an entrepreneur or a non-resident, you need to adjust these parameters.

1.3. Next, go to the “Information about the declarant” section. As soon as you select a section, it is highlighted in a different color. Initially, in this section you are asked to fill out your full name, date and place of birth, and an identification document.

1.4. After filling it out, you need to go to the page with information about your residence address. To do this, click on the house icon.

OKATO can be clarified at the inspection office at your place of residence.

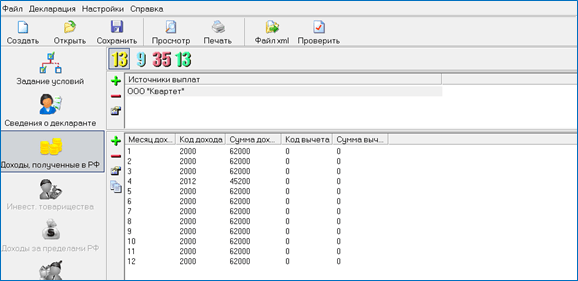

1.5. The next section is “Income received in the Russian Federation.” This section records all the income you receive: as per income certificates in form 2-NDFL, as well as income received from the sale, for example, of property owned for less than 3 years.

Initially, a section was allocated for income, taxable We wash at a rate of 13%. Basically, personal income is taxed at a rate of 13%. If you have other income, then fill out the sections with your existing rates in full.

1.6. Enter all sources of payments, that is, the names and details of the enterprises where you received income, in the “Source of payments” section. For each payment source, enter your monthly income. Enter information from 2-NDFL certificates. The total amount of income is calculated automatically. The remaining total amounts by payment source are entered manually from the certificate.

1.7. To enter the payment source, click the “+” icon. If you entered the payment source incorrectly and want to delete it, click “-“. If you want to change the payment source information, click .

1.8. When you click on the “+” icon, you are presented with a window for entering information:

1.9. Information “Name”, “TIN”, “KPP”, “OKATO” is entered from 2-NDFL certificates. At the same time, OKATO, which you indicated in the section “Newinformation about the declarant", may differ from OKATO, the indicationlisted in the certificate. This will be the case if you haveyou have a permanent residence permit in one locality, andyou work in another.

If, according to the 2-NDFL certificate, you were provided with standard deductions at your enterprise, check the box “Calculation of standard deductions from this source.” After entering the values, click Yes.

1.10. When entering the source of payments for the sale of property, if you do not know the details of the buyer, you can indicate in the “Name”, for example, “Sale of an apartment” or “Sale of a car.” In this case, the TIN and KPP are not filled out. OKATO must indicate the same as in the “Information about the declarant” section, that is, at the place of registration. Check mark in "Calculation" standard deductions according to this source" is not included. After entering the values, click Yes.

1.11. After entering all payment sources, go to enter income by month for each source. To do this, go to the next section. To enter information on the first payment source, click the “+” icon. If you entered the information incorrectly and want to delete it, click “-”. To edit information, click .

There is one more key in this section“Repeat income”, serves for duplicationthe same income information.

1.12. When you click on the “+” icon, you are presented with a window for entering information:

1.13. The system prompts you to select an income code from the directory. Since our first source of payments is “Car Sales,” the code is selected independently.

When selling a car, select code 1520, when selling an apartment - code 1510. Click “Yes”.

1.14. Enter the amount of income (the cost of the car) and the month the income was received (the month of sale). The button for selecting a deduction (expense) code becomes available.

1.15. Select the deduction code from the directory. Since the amount of the sale of a car owned for less than 3 years, in our case, is up to 250 thousand rubles, select the deduction code - “906”. As a result, the “Deduction Amount” will be automatically filled in with the value. Click Yes.

1.16. For the source of payments “Car sales”, information by month has been entered in full.

Now enter the information by month for the next payment source. This source is the company where you work. Enter the information from the 2-NDFL certificate, indicating the income and deduction codes that are reflected in the certificate.

1.17. By source of payments at the main place of work, information by month will look like this:

1.18. The last section to fill out is “Deductions”.

1.19. The icon panel allows you to take a page to fill out the necessary deductions.

1.20. Selecting the first icon opens a page for entering standard deductions. When choosing the second

- page for entering social deductions. If you select the third, there will be a page for entering property deductions when purchasing an apartment. If you select the latter, a page for entering deductions for losses with securities will appear.

1.21. Enter standard deductions by clicking on the first icon.

To calculate standard deductions, you need to check the “Provide standard deductions” box.

If you do not have special benefits for personal income tax, in your declarations before 2012, mark the code “No 104 and 105 deduction” with a dot (it is checked by default). If there are benefits, select either code 104 or code 105.

If you have children under 18 or full-time students under 24, enter the number of children in

corresponding lines.

The amount of deductions based on monthly income is calculated automatically by the program.

1.22. If you fill out a sales declaration same property, then filling out the declaration ends here. Go to point 4.

2. Filling out declaration sheets when receiving social deductions (treatment, training, voluntary pension insurance)

2.1. To enter expenses for training, treatment, ext. for voluntary pension insurance, click the icon in the “Deductions” section

An input page will open. Check the box “Provide social deductions.”

If you want to receive deduction for your education, enter the amount spent on training in the reporting year in the “Your training” line.

If deduction for treatment yourself, or parents, or children - enter the amount of expenses in the reporting year in the “Treatment” line.

If you want to receive deduction for children's education when teaching them full-time, click the “+” sign in the “Amounts paid for children’s education” block.

If deduction under a voluntary pension insurance agreement, click the “+” sign in the block of the same name.

2.2. To enter the amount spent on children’s education in the reporting year, click on the “+” sign in the block of the same name. After completing the entry, click "Yes".

To enter pension insurance amounts, a more complex form for entering contract data is offered. After entering, click "Yes".

If you have no other deductions, proceed to point 5.

3. Filling out additional sheets of the declaration tions when receiving a property deduction (according topurchase of an apartment, house, share of an apartment, interest on a loan for a purchased apartment)

3.1. To enter expenses for the purchase of an apartment, residential at home, click the icon in the “Deductions” section.

An input page will open.

Check the box " Provide property tax deduction».

Fill in all lines sequentially.

First, select the acquisition method: “purchase agreement” or “investment”. In the example, “purchase and sale agreement” is selected.

3.2. Select an object from the proposed list in the “Object name” line. For example, “apartment”:

3.3. Select the type of property from the list provided in the “Type of property” line. For example, “common shared property”

3.4. Select a taxpayer characteristic from the list provided in the “Taxpayer characteristic” line. For example, “object owner”.

3.5. Enter the address of the property; the date of the act, if the object is new, or the date of registration of the right; share, if shared ownership.

3.6. Enter the year you started using the deduction. It is equal to the year in which the apartment (or other object) was purchased.

3.7. Enter the amounts by clicking the "Proceed to enter amounts" button.

Enter the requested information and click the "Return to item details" button

4. Saving the declaration

4.1. If you don't have enough time to enter now 3-NDFL declaration in full, you can save it and fill out the declaration at any time. To do this, go to the "File" menu and select "Save As".

4.2. Select the directory on the local (or network) computer drive in which you want to save the declaration and enter the file name. The program offers the extension by default. For declarations for 2012 - extension *.dc2. Click the "Save" button.

4.3. Subsequently, when entering the program, so that Continue entering the declaration, select the “Open” menu item.

4.4. Select the saved file and click Open.

5. Recording the declaration on a flash card

5.1. To ensure that your declaration is completed quickly and without errors entered into the tax authorities’ database, generate a declaration electronically. To do this, select the top menu item “Export”:

5.2. Select the desired directory to save and click “Ok”.

5.3. A *.xml file will be generated:

5.4. Copy the generated *.xml file to a flash card or any other medium.

With a printed declaration, a file on a flash drive, certificates in form 2-NDFL and the necessary documents, come to the tax office.

03/20/2019, Sashka Bukashka

On February 18, 2018, the order of the Federal Tax Service of Russia dated October 25, 2017 N ММВ-7-11/822@ came into force, which introduced changes to the tax return form for personal income tax (form 3-NDFL). These changes are also valid in 2019 for declaring income received in 2018. Let's look at how to fill out the form taking into account the new requirements.

Personal income tax is a personal income tax paid to the state by working citizens, and is a declaration that is submitted to the tax service by people receiving income in Russia. This article describes how to fill out the 3-NDFL declaration and why it is needed.

Who needs to submit a tax return 3-NDFL

The declaration is submitted upon receipt of income on which personal income tax must be paid, as well as to return part of the tax previously paid to the state. 3-NDFL is submitted:

- Individual entrepreneurs (IP), lawyers, notaries and other specialists who earn their living through private practice. What these people have in common is that they independently calculate taxes and pay them to the budget.

- Tax residents who received income in other states. Tax residents include those citizens who actually live in Russia for at least 183 days a year.

- Citizens who received income from the sale of property: cars, apartments, land, etc.

- Persons who received income under a civil contract or from renting out an apartment.

- Lucky people who win the lottery, slot machines or betting must also pay tax on their winnings.

- If necessary, obtain a tax deduction: for, for, and so on.

Do not confuse this document with . They have similar names and usually come in the same set of documents, but they are still different.

Where to file the 3-NDFL declaration

The declaration is submitted to the tax service at the place of permanent or temporary registration (registration). It is handed over in person or sent by mail. You can also submit your tax return online. To fill out 3-NDFL online, obtain a login and password to enter the taxpayer’s personal account at any tax office. To receive your login and password, come in person and don’t forget your passport.

Deadlines for filing 3-NDFL in 2019

In 2019, the personal income tax return in Form 3-NDFL is submitted by April 30. If the taxpayer completed and submitted the report before the amendments to the form came into force, he does not need to submit the information again using the new form. If you need to claim a deduction, you can submit your return at any time during the year.

Sample of filling out 3-NDFL in 2019

You will be assisted in filling out the 3-NDFL declaration by the “Declaration” program, which can be downloaded on the website of the Federal Tax Service. If you fill out 3-NDFL by hand, write text and numeric fields (TIN, fractional fields, amounts, etc.) from left to right, starting from the leftmost cell or edge, in capital printed characters. If after filling out the field there are empty cells, dashes are placed in them. For a missing item, dashes are placed in all cells opposite it.

When filling out the declaration, no mistakes or corrections should be made; only black or blue ink is used. If 3-NDFL is filled out on a computer, then the numerical values are aligned to the right. You should print in Courier New font with a size set from 16 to 18. If you do not have one page of a section or sheet of 3-NDFL to reflect all the information, use the required number of additional pages of the same section or sheet.

Amounts are written down indicating kopecks, except for the personal income tax amount, which is rounded to the full ruble - if the amount is less than 50 kopecks, then they are discarded, starting from 50 kopecks and above - rounded to the full ruble. Income or expenses in foreign currency are converted into rubles at the exchange rate of the Central Bank of the Russian Federation on the date of actual receipt of income or expenses. After filling out the required pages of the declaration, do not forget to number the pages in the “Page” field, starting from 001 to the required one in order. All data entered in the declaration must be confirmed by documents, copies of which must be attached to the declaration. To list documents attached to 3-NDFL, you can create a special register.

Instructions for filling out 3-NDFL. Title page

A cap

In the “TIN” paragraph on the title and other completed sheets, the identification number of the taxpayer - an individual or company - is indicated. In the item “Adjustment number”, enter 000 if the declaration is submitted for the first time this year. If you need to submit a corrected document, then 001 is written in the section. “Tax period (code)” is the period of time for which a person reports. If you are reporting for a year, enter the code 34, the first quarter - 21, the first half of the year - 31, nine months - 33. “Reporting tax period” - in this paragraph, indicate only the previous year, the income for which you want to declare. In the “Submitted to the tax authority (code)” field, enter the 4-digit number of the tax authority with which the submitter is registered for tax purposes. The first two digits are the region number, and the last two are the inspection code.

Taxpayer information

In the “Country Code” section, the code of the applicant’s country of citizenship is noted. The code is indicated according to the All-Russian Classifier of Countries of the World. The code of Russia is 643. A stateless person marks 999. “Taxpayer category code” (Appendix No. 1 to the procedure for filling out 3-NDFL):

- IP - 720;

- notary and other persons engaged in private practice - 730;

- lawyer - 740;

- individuals - 760;

- farmer - 770.

The fields “Last name”, “First name”, “Patronymic”, “Date of birth”, “Place of birth” are filled in exactly according to the passport or other identity document.

Information about the identity document

The item “Document type code” (Appendix No. 2 to the procedure for filling out 3-NDFL) is filled in with one of the selected options:

- Passport of a citizen of the Russian Federation - 21;

- Birth certificate - 03;

- Military ID - 07;

- Temporary certificate issued instead of a military ID - 08;

- Passport of a foreign citizen - 10;

- Certificate of consideration of an application to recognize a person as a refugee on the territory of the Russian Federation on its merits - 11;

- Residence permit in the Russian Federation - 12;

- Refugee certificate - 13;

- Temporary identity card of a citizen of the Russian Federation - 14;

- Temporary residence permit in the Russian Federation - 15;

- Certificate of temporary asylum in the Russian Federation - 18;

- Birth certificate issued by an authorized body of a foreign state - 23;

- Identity card of a Russian military personnel/Military ID of a reserve officer - 24;

- Other documents - 91.

The items “ ”, “Date of issue”, “Issued by” are filled out strictly according to the identity document. In “Taxpayer Status,” number 1 means a tax resident of the Russian Federation, 2 means a non-resident of Russia (who lived less than 183 days in the Russian Federation in the year of income declaration).

Taxpayer phone number

In the new form 3-NDFL, fields for indicating the taxpayer’s address have been removed. Now you do not need to indicate this information on the form. Simply fill out the “Contact phone number” field. The telephone number is indicated either mobile or landline, if necessary, with the area code.

Signature and date

On the title page, indicate the total number of completed pages and the number of attachments - supporting documents or their copies. In the lower left part of the first page, the taxpayer (number 1) or his representative (number 2) signs the document and indicates the date of signing. The representative must attach a copy of the document confirming his authority to the declaration.

3 main mistakes in 3-NDFL that we usually make

Expert commentary specifically for Sashka Bukashka’s website:

Evdokia Avdeeva

StroyEnergoResurs, chief accountant

The most common errors can be divided into three groups:

- Technical errors. For example, a taxpayer forgets to sign on required sheets or skips sheets. The tax office will also refuse to provide deductions without supporting documents. The costs of purchasing property, treatment, training, insurance must be confirmed by contracts and payment documents.

- Incorrect or incomplete filling of data. “Top” of such shortcomings:

- on the title page in the line “adjustment number” when submitting the declaration for the first time, put 1, but it should be 0;

- incorrect OKTMO code.

Such shortcomings are not so terrible, and in the worst case they will lead to refusal to accept the declaration. But incompletely filling out some data can lead to the tax office “misunderstanding you” and instead of providing a deduction, it will require you to pay tax.

For example, if the taxpayer in the section “Income received in the Russian Federation” does not indicate the amount of income, the amount of tax calculated and the amount of tax withheld, then instead of refunding the tax, the taxpayer will calculate it for himself as an additional payment.

- Ignorance of laws and rules for applying deductions. For example, a citizen paid for training in 2017, but wants to receive a deduction for 2018. However, the tax benefit is provided specifically for the year in which the applicant paid for education, medical care or other services.

Filling out 3-NDFL when declaring income and filing tax deductions

The procedure for filling out 3-NDFL depends on the specific case for which you are filing a declaration. The declaration form contains 19 sheets, of which you need to fill out the ones you personally need.

- Section 1 “Information on the amounts of tax subject to payment (addition) to the budget/refund from the budget”;

- Section 2 “Calculation of the tax base and the amount of tax on income taxed at the rate (001)”;

- sheet A “Income from sources in the Russian Federation”;

- sheet B “Income from sources outside the Russian Federation, taxed at the rate (001)”;

- sheet B “Income received from business, advocacy and private practice”;

- sheet D “Calculation of the amount of income not subject to taxation”;

- Sheet D1 “Calculation of property tax deductions for expenses on new construction or acquisition of real estate”;

- Sheet D2 “Calculation of property tax deductions for income from the sale of property (property rights)”;

- sheet E1 “Calculation of standard and social tax deductions”;

- sheet E2 “Calculation of social tax deductions established by subparagraphs 4 and 5 of paragraph 1 of Article 219 of the Tax Code of the Russian Federation”;

- sheet J “Calculation of professional tax deductions established by paragraphs 2, 3 of Article 221 of the Tax Code of the Russian Federation, as well as tax deductions established by paragraph two of subparagraph 2 of paragraph 2 of Article 220 of the Tax Code of the Russian Federation”;

- sheet 3 “Calculation of taxable income from transactions with securities and transactions with derivative financial instruments”;

- Sheet I “Calculation of taxable income from participation in investment partnerships.”

In addition to paying personal income tax, the declaration will be useful to receive a tax deduction. By law, every citizen can return part of the tax previously paid to the state to cover the costs of education, treatment, purchase of real estate or payment of a mortgage loan. You can submit documents to receive a deduction any day after the end of the year in which the money was spent. The deduction can be received within three years.